September 20, 2022

The home of the Federal Reserve Bank is on Constitution Avenue in Washington, DC. That’s just a few blocks away from our headquarters so we speak from experience when we say: As the Fed considers a historic third 75 basis point increase, it’s quiet on Constitution Avenue. FOMC participants have clearly stated they will raise rates higher and hold them high for as long as it takes. Not much discussion needed at this meeting. Perhaps: Should we go up 100 basis points? But it will be the review of the surprisingly strong August CPI reading and turn in your economic estimates for the DOT plot. We expect plenty of tough talk from the Chairman at his press conference on Wednesday, including warnings of recession, and not a care about market volatility.

Why? Let’s review the four scenarios we predict could happen in the near term:

1. The Fed defeats inflation

2. A recession happens

3. Volatility increases

4. inflation remains hot and the economy continues growing

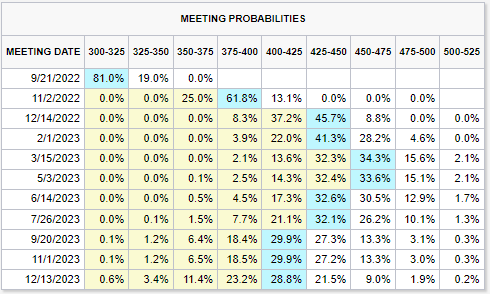

The first three scenarios, the Fed might ease rates and long rates might comes down. But given the latest economic readings, the fourth scenario seems to be winning. But we ask ourselves, is that sustainable? Since the release of the August CPI report, the CME Fed Watch Tool (Below) now anticipates the Fed raising rates, September (75 bps), November (75 bps) and December (50 bps) to end the year at 4.25-4.50%. The futures also show the Fed will keep rates around that 4-4.5% level for most of 2023. The Fed can’t do anything to fix the supply chain, but they can and will do something about demand for those supplies.

As we look closely at those scenarios, we see two themes for fixed income. Credit spreads could continue to widen. Credit spreads are above long-term averages, but not quite at recession or crisis levels and there is still room to widen. Long term rates, while volatile in the immediate term, could start to come down as soon as the Fed signals they are done raising rates. We are closing in on the 4th quarter of 2022. 2023 will bring in a new investment thesis that will include a new outlook on rates. We think that outlook could be for lower rates as the Fed either won or went too far.

-Peter Baden, CFA

Chief Investment Officer

Click on the above links for more information on important investment and economic concepts.

Click on the above links for more information on important investment and economic concepts.

CME Fed Watch Tool

Source: https://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html

Contact Genoa Asset Management

William (Kip) Weese

SVP, Intermediary Sales

Northeast & South West

(508) 423-2269

Email Kip

Art Blackman

VP, Intermediary Sales

Central

(816) 688-8482

Email Art

Rick Bell

VP, Intermediary Sales

North Central & North West

(513) 762-3694

Email Rick

Disclosures

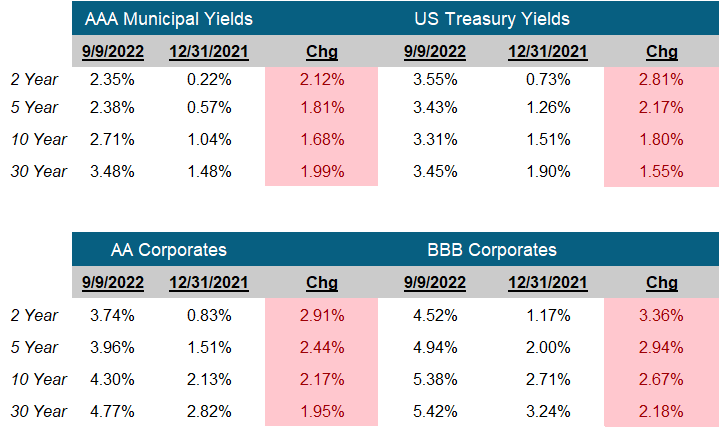

Indexes used for AAA Municipal Yields

2 Year: BVAL Municipal AAA Yield Curve (Callable) 2 Year (Symbol: CAAA02YR BVLI)

5 Year: BVAL Municipal AAA Yield Curve (Callable) 5 Year (Symbol: CAAA04YR BVLI)

10 Year: BVAL Municipal AAA Yield Curve (Callable) 10 Year (Symbol: CAAA10YR BVLI)

30 Year: BVAL Municipal AAA Yield Curve (Callable) 30 Year (Symbol: CAAA30YR BVLI)

Indexes used for US Treasury Yields

2 Year: US Generic Govt 2 Year Yield (Symbol: USGG2YR)

5 Year: US Generic Govt 5 Year Yield (Symbol: USGG5YR)

10 Year: US Generic Govt 10 Year Yield (Symbol: USGG10YR)

30 Year: US Generic Govt 30 Year Yield (Symbol: USGG30YR)

F/m Investments, LLC, doing business as Genoa Asset Management (Genoa), is an investment advisor registered under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. For more information please visit: https://adviserinfo.sec.gov/ and search our firm name. The opinions expressed herein are those of Genoa and may not come to pass. The material is current as of the date of this presentation and is subject to change at any time, based on market and other conditions. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. The information presented does not involve the rendering of personalized financial, legal or tax advice, but is limited to the dissemination of general information for educational purposes. Please consult financial, legal or tax professionals for specific information regarding your individual situation. This information does not constitute a solicitation or an offer to buy or sell any securities. Although taken from reliable sources, Genoa cannot guarantee the accuracy of the information received from third parties. Charts, diagrams, and graphs, by themselves, cannot be used to make investment decisions. Investing involves risk of loss, including loss of principal. Past performance is no guarantee of future results. An index is a portfolio of specific securities, the performance of which is often used as a benchmark in judging the relative performance of certain asset classes. Indexes are unmanaged portfolios and investors cannot invest directly in an index. An index does not charge management fees or brokerage expenses, and no such fees or expenses were deducted from the performance shown.