November 4, 2022

Wednesday afternoon the Fed Statement came out and it seemed, reading between the lines, that perhaps the Fed was changing their tune (Dare we say, Relenting?). As the market breathed a sigh of relief, the press conference started, and we found out Chairman Powell and the Fed are Relentless.

To summarize the Chairman: The time to slow down is coming and may be at the next meeting but that is not decided yet. More important now is how high the terminal rate will be and how long we maintain that rate. He also stated: the cumulative effect of the rate increases happens with a lag, but he needs to see inflation come down “Decisively” before they will change course. He also talked about solving the problem of “Over-tightening” is easier than “Under-Tightening”. Finally, he said the window for a soft landing had narrowed, but not closed.

So, the Fed did pivot, just not the way the market wanted. They pivoted from large rate hikes to more, smaller rate hikes, ending at a rate “Higher than we communicated last meeting”. Why? The Economy. Third quarter GDP was strong. October Employment was strong with Non-Farm payrolls surprisingly strong and the Unemployment rate at 3.7%. Not to mention the JOLTs report shows there are still more jobs open than we have unemployed to fill them. All this is strength is keeping inflation hot as shown in the September CPI numbers (See below).

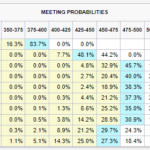

Currently, the CME Fed Watch Tool indicates the Fed will increase 75 bps at the December 14th meeting, 50 bps in February and 25 bps in March of next year. While not showing signs of relenting, the market does seem to think the Fed will do those three hikes and with a terminal rate around the 5.00-5.25% level. The last time we were at 5%? 2006, when the Fed cycle topped out at 5.25%.

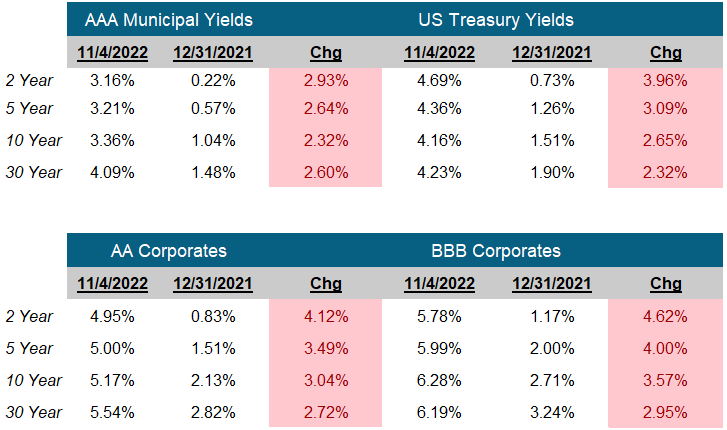

We are still concerned that problems in the global financial system could make our potentially mild recession worse, but rates are attractive today. US Treasuries are at levels not seen since 2007. Looking at the 1-year break even yield on the 2-Year US Treasury (The yield a 1 Year Treasury would need to trade at 12 months from now to lose money), is now 9.8%. Stated a different way, you can buy a 2-year US Treasury today with a yield to maturity of 4.67% and make money over the next twelve months if the 1-Year yield to maturity stays below 9.8%. We believe that is a good balance of risk and reward.

-Peter Baden, CFA

Chief Investment Officer

Click on the above links for more information on important investment and economic concepts.

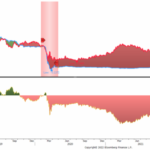

Consumer Price Index Ex Food & Energy

Monthly for the last 30 years ended 9-30-22

Contact Genoa Asset Management

William (Kip) Weese

SVP, Intermediary Sales

Northeast & South West

(508) 423-2269

Email Kip

Art Blackman

VP, Intermediary Sales

Central

(816) 688-8482

Email Art

Rick Bell

VP, Intermediary Sales

North Central & North West

(513) 762-3694

Email Rick

Disclosures

Indexes used for AAA Municipal Yields

2 Year: BVAL Municipal AAA Yield Curve (Callable) 2 Year (Symbol: CAAA02YR BVLI)

5 Year: BVAL Municipal AAA Yield Curve (Callable) 5 Year (Symbol: CAAA04YR BVLI)

10 Year: BVAL Municipal AAA Yield Curve (Callable) 10 Year (Symbol: CAAA10YR BVLI)

30 Year: BVAL Municipal AAA Yield Curve (Callable) 30 Year (Symbol: CAAA30YR BVLI)

Indexes used for US Treasury Yields

2 Year: US Generic Govt 2 Year Yield (Symbol: USGG2YR)

5 Year: US Generic Govt 5 Year Yield (Symbol: USGG5YR)

10 Year: US Generic Govt 10 Year Yield (Symbol: USGG10YR)

30 Year: US Generic Govt 30 Year Yield (Symbol: USGG30YR)

F/m Investments, LLC, doing business as Genoa Asset Management (Genoa), is an investment advisor registered under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. For more information please visit: https://adviserinfo.sec.gov/ and search our firm name. The opinions expressed herein are those of Genoa and may not come to pass. The material is current as of the date of this presentation and is subject to change at any time, based on market and other conditions. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. The information presented does not involve the rendering of personalized financial, legal or tax advice, but is limited to the dissemination of general information for educational purposes. Please consult financial, legal or tax professionals for specific information regarding your individual situation. This information does not constitute a solicitation or an offer to buy or sell any securities. Although taken from reliable sources, Genoa cannot guarantee the accuracy of the information received from third parties. Charts, diagrams, and graphs, by themselves, cannot be used to make investment decisions. Investing involves risk of loss, including loss of principal. Past performance is no guarantee of future results. An index is a portfolio of specific securities, the performance of which is often used as a benchmark in judging the relative performance of certain asset classes. Indexes are unmanaged portfolios and investors cannot invest directly in an index. An index does not charge management fees or brokerage expenses, and no such fees or expenses were deducted from the performance shown.